For years, homeowners insurance was treated as a routine line item in the cost of homeownership.

Not anymore.

Today, insurance costs are becoming one of the fastest-growing expenses impacting homeowners, lenders, servicers, investors, and residential portfolio operators nationwide.

According to the U.S. Department of the Treasury, homeowners insurance premiums are rising across the country, with higher-risk ZIP codes paying substantially more than lower-risk areas. The Treasury also found that policy nonrenewals are increasing in high-risk regions, making coverage harder to obtain in some markets.

Meanwhile, a report from the U.S. Government Accountability Office found that homeowners insurance availability and affordability continue to be major concerns, particularly in areas exposed to natural disaster risk.

The conversation has shifted.

It's no longer just:

"Can this property get insured?"

Now the question is:

"Can we verify the property's condition quickly enough to support underwriting decisions before risk becomes a problem?"

For carriers, the stakes are significant.

A roof nearing the end of its useful life, unreported storm damage, deferred maintenance, or emerging safety hazards can materially impact underwriting decisions, renewal eligibility, and claim exposure.

Yet many organizations are still making those decisions without current property-level visibility.

Property-Level Risk Is Reshaping Underwriting

Insurance carriers are moving beyond ZIP-code-level risk analysis.

Today's underwriting environment increasingly relies on property-specific characteristics such as roof condition, roof age, exterior maintenance, storm damage, vegetation encroachment, occupancy status, deferred maintenance, and visible signs of deterioration.

Matic's insurance market analysis found that roof age continues to play a growing role in underwriting and pricing decisions, with premium differences widening significantly between newer and aging roofs.

In other words, two homes on the same street may receive very different insurance outcomes based solely on property condition.

That creates a significant challenge for carriers, servicers, investors, and single-family rental operators managing hundreds or thousands of properties.

You can't manage risk if you can't see it.

Historically, obtaining current property condition data meant scheduling inspections, coordinating access, managing multiple vendors, waiting days or weeks for results, and reviewing inconsistent reporting formats.

When multiplied across large residential portfolios, those delays can impact underwriting timelines, policy renewals, risk mitigation efforts, and operational efficiency.

As insurance carriers become increasingly selective, access to current, verifiable property intelligence is becoming essential.

How Insurers Are Closing the Property Visibility Gap

The challenge isn't a lack of data.

It's a lack of current, verifiable data.

When an underwriter is evaluating a property, a servicer is reviewing a portfolio, or a carrier is assessing renewal risk, decisions are often being made using information that may be months or even years old.

A roof may have deteriorated.

Storm damage may have occurred.

Deferred maintenance may have accelerated.

Occupancy may have changed.

Without current property intelligence, organizations are left making risk decisions with an incomplete picture.

Whether an insurer needs to verify roof condition before renewal, assess storm-related damage after a weather event, validate occupancy, or monitor property condition across a residential portfolio, obtaining current field intelligence has traditionally required coordinating inspectors, managing vendors, and waiting days for results.

ProxyPics streamlines that process by enabling real-time property data collection nationwide through a network of more than 420,000 data collectors.

Businesses can obtain property condition documentation, occupancy verification, disaster assessments, insurance inspections, custom surveys, View360, videos, and other property intelligence without deploying their own field workforce.

But speed alone isn't enough.

In an industry where fraud prevention, auditability, and data integrity are critical, every submission is tied to multiple layers of verification. Photos are captured within designated geofenced areas, GPS coordinates are recorded, timestamps are embedded, and submissions pass through quality control review before delivery.

The result is a documented chain of custody for the property data itself.

Instead of relying on outdated records, satellite imagery, or assumptions, clients receive verifiable field intelligence captured at the property and delivered in a format that supports underwriting, risk assessment, portfolio monitoring, and operational decision-making.

As insurance carriers place greater emphasis on property-specific risk factors, access to current field data is becoming less of a competitive advantage and more of an operational necessity.

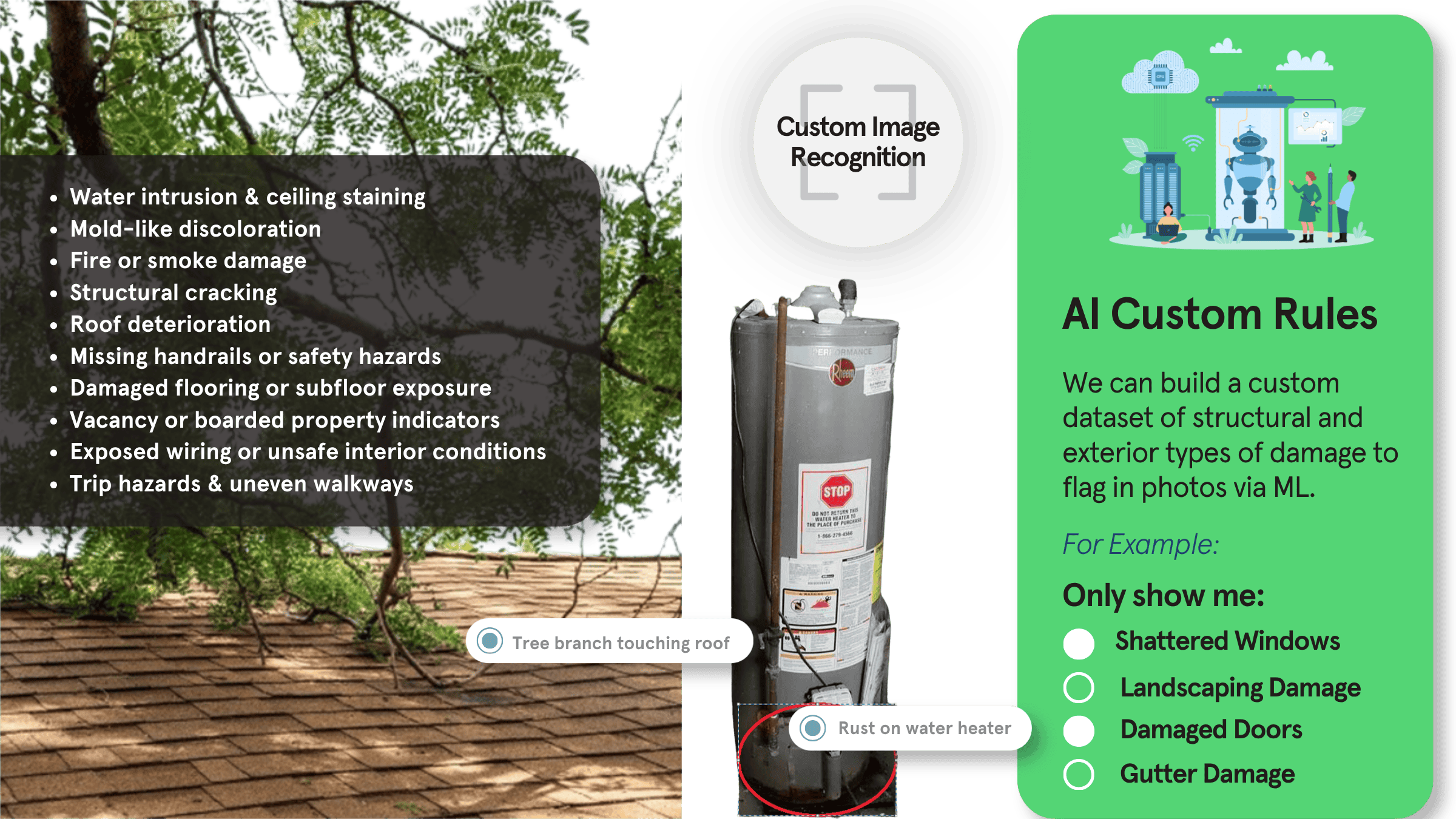

AI Is Helping Surface Risks Before They Become Claims

Capturing current property intelligence solves one challenge.

Understanding what that data means at scale is another.

Insurance carriers, servicers, and portfolio operators often review thousands of properties across multiple markets. As the volume of property imagery grows, manually identifying potential risks, maintenance concerns, or underwriting red flags becomes increasingly difficult.

A carrier reviewing 500 properties doesn't need more photos.

They need faster ways to identify which properties deserve attention first.

That's where AI is beginning to change the conversation.

ProxyPics utilizes AI models designed to analyze field-collected property imagery and surface observable conditions that may warrant additional review.

Rather than replacing human review, AI serves as an additional layer of analysis that helps identify patterns, conditions, and risk indicators that may otherwise be overlooked during high-volume review processes.

For underwriting teams, this can help accelerate reviews.

For insurers, it can support more informed risk assessments.

For portfolio operators, it can provide earlier visibility into issues that may impact asset performance, maintenance costs, or future insurability.

When combined with real-time field data, GPS validation, geofencing controls, and quality assurance review, AI helps transform property documentation into actionable property intelligence.

Because in today's insurance environment, the organizations that can identify risk faster are often the organizations that can manage it more effectively.

Why This Matters for Residential Portfolios

For mortgage servicers, insurers, investors, and single-family rental operators, property condition visibility directly impacts risk management.

Without current field data, organizations may struggle to identify:

- Emerging maintenance issues

- Storm-related damage

- Vacancy concerns

- Property deterioration

- Insurance eligibility concerns

- Compliance risks

As insurance carriers continue tightening underwriting requirements and homeowners face increasing premium pressure, having access to current property intelligence becomes less of a convenience and more of a necessity.

Organizations that can proactively identify issues before they become claims, losses, or costly repairs are often better positioned to protect assets and make informed decisions.

The Future of Insurance Starts With Better Property Data

Rising insurance premiums aren't simply an insurance problem.

They're a property visibility problem.

The insurance industry has spent years building increasingly sophisticated risk models.

Those models are only as reliable as the property data feeding them.

As underwriting becomes increasingly property-specific, organizations that can verify conditions quickly, consistently, and at scale will be better positioned to manage risk, improve decision-making, and respond to a rapidly changing insurance landscape.

Current property intelligence is no longer a nice-to-have. It's becoming a critical component of modern underwriting, portfolio management, and risk assessment.

If property visibility is becoming a challenge for your organization, let's have a conversation.