A Chicago homeowner lost access to her home after her front porch stairs collapsed following a brutal winter. What should have been a straightforward insurance claim quickly turned into something far more complicated and far more concerning.

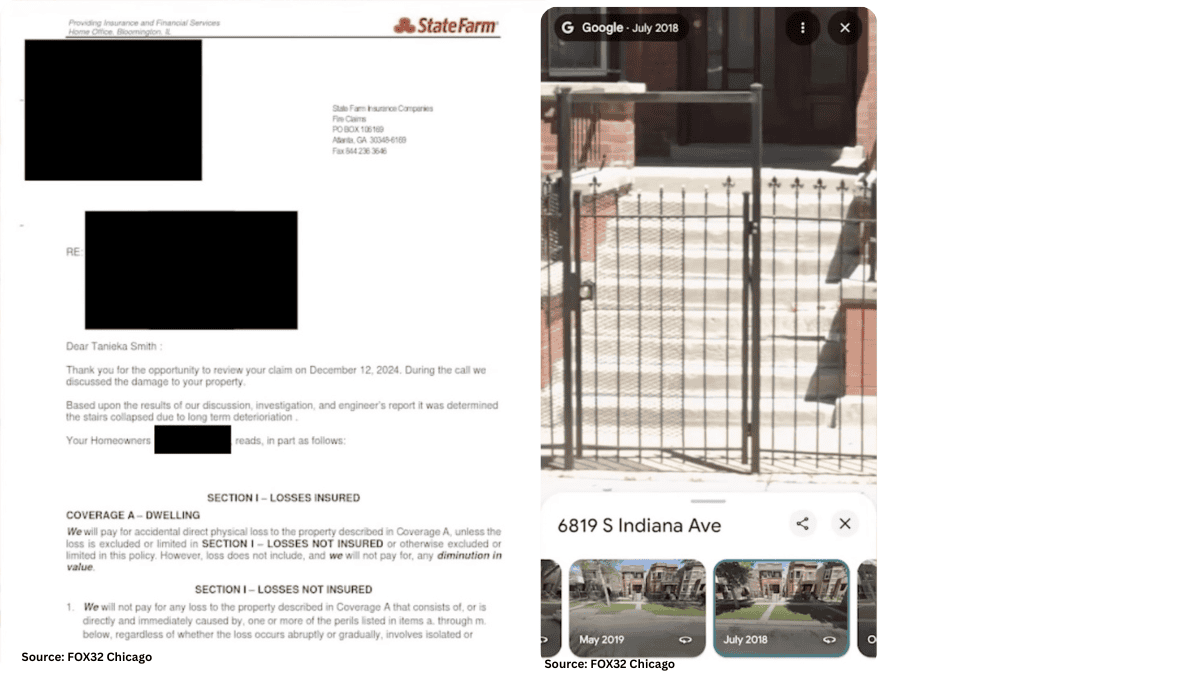

After filing her claim and waiting months for a response, she received a denial. Not based on a recent inspection. Not based on a field report. Instead, the decision pointed to publicly available Google Images.

According to FOX 32 Chicago, the insurer referenced Google imagery from 2022 to support the claim that the damage may have already existed.

At first glance, that might seem reasonable. Until you look closer.

The Detail That Changes the Entire Narrative

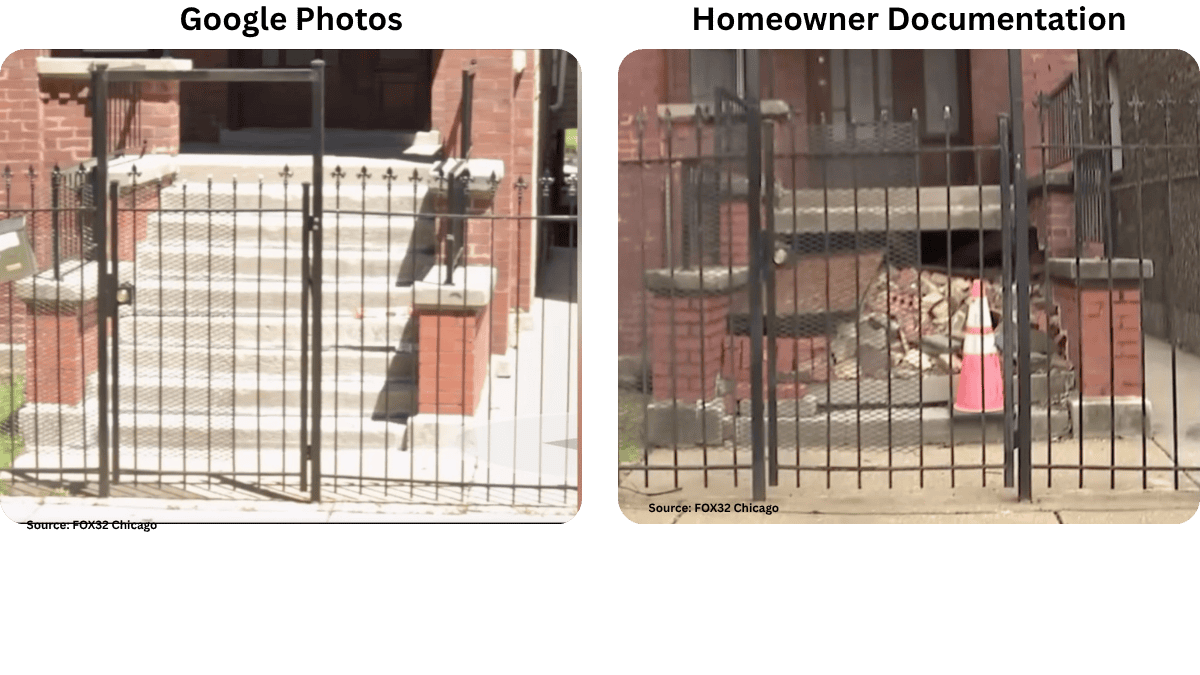

The homeowner didn’t accept the denial at face value. She went back and pulled her own records, looking at the same source being used against her.

What she found complicates everything.

She identified Google images from 2018 and 2019 that showed the same condition of the stairs, with no visible changes leading up to the 2022 image used in the denial.

Her position is simple, but it exposes a deeper issue:

If the condition truly existed before the policy was active, why was the home insured without that being flagged?

That question doesn’t just challenge the claim decision. It challenges the consistency of the entire process, from underwriting to claims handling.

This Isn’t About Google Images. It’s About the Data Behind the Decision.

It’s easy to focus on the use of Google Images, but that misses the bigger point. The real issue is what happens when decisions rely on data that was never intended to support them.

Google Images were not captured:

- At the time of loss

- Under any inspection standard

- With full visibility of the structure

- With a verifiable audit trail tied to a claim

So while they can offer context, they cannot offer certainty.

And in claims, certainty is what everything hinges on.

Where the Process Breaks Down

When you step back, this case highlights a pattern that shows up across the industry more often than people admit.

There are three points where things tend to fall apart:

1. The starting condition is unclear

If there is no structured documentation at the time of underwriting, every future comparison becomes subjective. What looks like “pre-existing damage” could just as easily be long-standing but accepted condition.

2. The moment of loss is not properly captured

Without immediate, on-site documentation, the claim relies on whatever data happens to be available. That often means outdated imagery or incomplete views of the property.

3. The decision lacks defensible support

When a claim is challenged, the data used needs to hold up. If it can be contradicted by pulling from the same public source, it loses credibility quickly.

This is how situations shift from evaluation to dispute.

What a Defensible Approach Actually Looks Like

If the right data had been in place, this situation likely would not have escalated the way it did. The conversation would not revolve around interpreting images. It would revolve around verified facts.

A stronger approach includes:

- A clear, documented condition of the property at policy inception

- A rapid response to capture the condition immediately after the incident

- Geotagged and timestamped images tied to a single, validated session

- A complete set of required photos that show structural elements in detail

- A consistent format that allows for direct comparison over time

When those elements exist, decisions become easier to make and harder to challenge.

How ProxyPics Addresses This Gap

This is where the difference between generic imagery and purpose-built data becomes clear.

ProxyPics was designed to support situations exactly like this, where timing, accuracy, and verification matter. Instead of relying on whatever images are available, the platform enables teams to capture what they actually need, when they need it.

With ProxyPics, teams can:

- Dispatch a local data collector to the property, often the same day, to capture current conditions

- Use guided self-inspections when access is limited, ensuring the right data is still collected

- Capture geotagged and timestamped images tied to a specific visit

- Follow structured inspection templates aligned to underwriting or claims requirements

- Run AI-supported checks before delivery to ensure nothing critical is missed

The result is not just more data. It is better data, captured with the purpose of supporting real decisions.

The Bigger Risk This Case Brings to Light

What makes this situation stand out is not just the denial. It is how easily the reasoning behind it can be challenged.

When a homeowner can point to the same source of data and tell a different story, it creates friction that slows everything down. Claims take longer. Disputes increase. Confidence in the process starts to erode.

And all of it comes back to one core issue:

The data was never built to support the decision it was used for.

The Bottom Line

Google Images are accessible and convenient, but they were never intended to serve as the foundation for underwriting or claims decisions.

As this case shows, convenience can quickly turn into vulnerability when the data lacks context, timing, and verification.

At the end of the day, the question is not whether the image exists.

It is whether the data can stand behind the decision.

See What Verified Property Data Looks Like

If your current process relies on static or third-party imagery, it may be time to rethink how property conditions are captured and validated.

See how real-time, structured property data can support stronger, faster decisions. Start below.